May 2026 Market Update

- Steven Reinisch

- May 29

- 5 min read

At the May FOMC meeting the committee once again decided to leave interest rates unchanged at 3.50%-3.75%. Over the past month the level of bank reserves (blue) in the chart below has risen as the Federal Reserve's balance sheet (orange) stayed relatively the same. The plumbing in the financial system continues to be extremely dependent on the small asset purchase program (QE) the Fed began at the December 2025 FOMC meeting. The small asset purchase program will have to grow much larger in the months ahead to support a deteriorating consumer economy, which has already and will continue to exacerbate inflation and affordability conditions consumers are experiencing.

Reserve Balances and Federal Reserve Balance Sheet

The new Federal Reserve Chairman has officially taken the reigns, and while many feel conditions in the economy warrant cutting interest rates, inflation data and energy supply shortages suggest otherwise. It will be interesting to see how Kevin Warsh, who wants to shrink the Feds balance sheet, deals with rising inflation, struggling consumer affordability, a weakening employment market, and energy supply shortages in the months ahead.

Lets take a look at some important economic data.

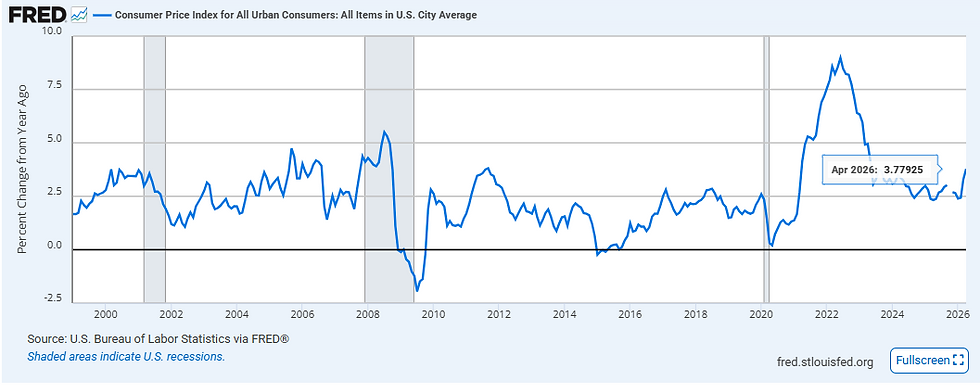

Inflation Rate - Consumer Price Index

Hiring Rate

Construction Hiring Rate

Newly Constructed Completed Homes for Sale

U.S. Personal Savings Rate

Real Personal Disposable Income

U.S. Real Personal Income Growth Rate

U.S. Real Wage Growth

Real Average Hourly Earnings Growth

American households are getting squeezed with rising costs for energy, housing, and healthcare. The U.S, savings rate fell to 2.6% in April, one of the lowest readings in history. Real personal income growth rate has fallen into negative territory (-1%). Real disposable income growth has turned negative and real average hourly earnings growth is also negative. Since 1960, there have only been 10 periods where the real personal income growth rate fell into negative territory, 8 out of 10 of those periods coincided with an economic recession.

University of Michigan Consumer Sentiment

University of Michigan Index of Consumer Confidence continues to bump against an all-time low, even as the stock market keeps making new all-time highs. In years past consumer sentiment and the stock market would rise and fall together, but now as the economy has become extremely dependent on deficit spending from the government and Ai capital expenditure spending, the U.S. economy and American households have become more dependent on the stock market than ever before. The government will do whatever it takes to keep asset prices such as real estate and stocks up. Even if that means ruining the purchasing power of the wages working Americans earn. Investment Advisers and Stock Index Managers have in a strange way become government employees under this new paradigm.

Household and Nonprofit Organizations Held Corporate Equities as a Percentage of Financial Assets

An unprecedented amount of gambling and complacency is taking place. The market believes if stock prices decline the government will quickly increase spending and/or the Fed will increase its balance sheet to keep money flowing and credit creation expanding no matter what the cost to the rest of the economy. The only way interest rates and mortgage rates are going to substantially decline is with a strong economic downturn and/or recession, combined with fiscal discipline. The next time the stock market and the economy declines, and the government quickly responds by printing money, interest rates/mortgage rates may actually rise rather than decline.

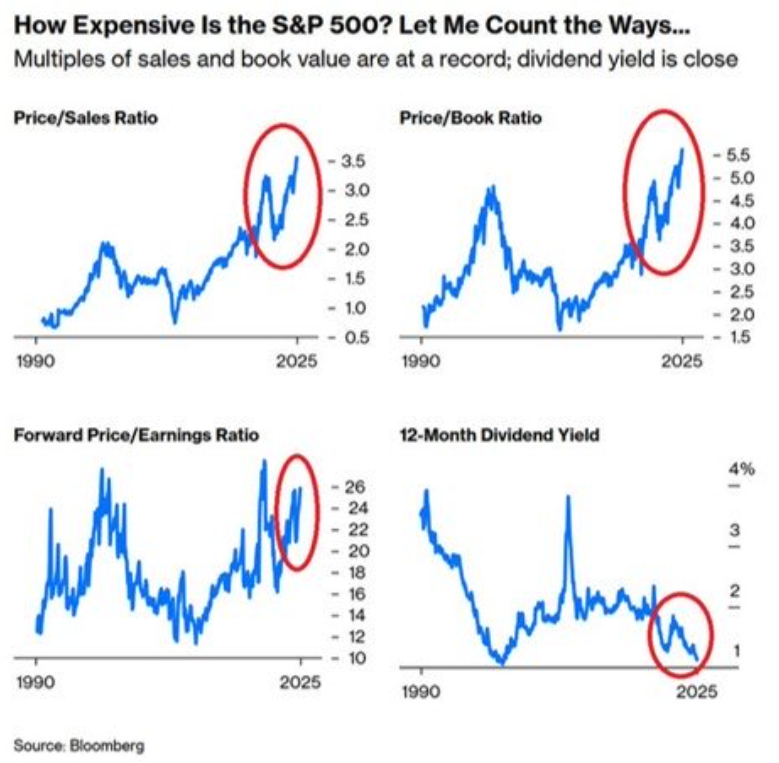

As previously mentioned in the April market update, an economic transition is underway, and there is high complacency in financial markets amidst extremely high stock and real estate market valuations. For those who do not understand the real economy, its true problems, and believe all is well simply because the prices of assets such as stocks and real estate are up, the following charts are important to consider when choosing their asset allocation mix. Investing in the S&P 500 at a price to earnings ratio of 22x or greater has historically led to a negative 10-year return. The valuation at which an investor enters the stock market significantly matters to their performance and return.

S&P 500 10 Year P/E Ratio & Buffett Indicator Standard Deviation from Long Term Trend

S&P500 Valuation Metrics - Bloomberg

Our MacroVex Capital, S&P 500 fair value estimate model currently indicates fair value for 2025 earnings of $272 and 2026 earnings of $312 between 4,155 and 4,920, down -45% and -35% from the S&P 500, 2026 May closing price of 7,580.

We believe throughout the rest of 2026 there will be major fiscal and monetary changes that provide great investment opportunities. Our recommendation is to position portfolios to endure a recession, in a defensive manor, risk off, cash, T-bills, money market funds, short to mid-term 1-10 year U.S. treasury bonds and 10-30 year U.S. treasury bonds at positive carry, 10-year minus 2-year yield curve re-steepening, 10-year minus 3-month yield curve re-steepening, Short USDJPY from 153, and select low duration U.S. equities.

Getting paid to wait for growth assets to be priced at discounts, while being positioned to benefit from bond price appreciation as interest rates decline from downward economic pressure, continues to be a profitable and rewarding strategy. We remain patient and focused on managing risk through 2026.

Disclosure: Investing involves risk, including the possible loss of principal and fluctuation of value. Past performance is no guarantee of future results. This letter is not intended to be relied upon as forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date noted and may change as subsequent conditions vary. The information and opinions contained in this letter are derived from proprietary and nonproprietary sources deemed by Macrovex Capital, LLC to be reliable. The letter may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projection, and forecasts. There is no guarantee that any forecast made will materialize. Reliance upon the information in this letter is at the sole discretion of the reader. Please consult with a Macrovex Capital, LLC financial advisor to ensure that any contemplated transaction in any securities or investment strategy aligns with your overall investment goals, objectives, and tolerance for risk. Additional information about Macrovex Capital, LLC is available in its current disclosure documents, Form ADV and Form ADV Part 2A Brochure, which are accessible online via the SEC’s investment Adviser Public Disclosure (IAPD) database at www.adviserinfo.sec.gov, using CRD #300692. Macrovex Capital, LLC is neither an attorney nor an accountant, and no portion of this content should be interpreted as legal, accounting or tax advice

Comments